How To Save Thousands On Your Mortgage!

This post contains Affiliate Links, which means at No Additional Cost to you, I receive a small commission if you purchase through these links. I do my utmost too be honest about the products I promote; however, I am not liable for any purchases made from these parties. See my Disclosure & Disclaimer Page for more details.

Over the years, I have learned some hard lessons from the Mortgage Industry. Everything from an Adjustable Rate Lock to Private Mortgage Insurance has taught me a few things. After a conversation with my brother, he pointed out that by the time you pay for your home, it's almost double the sale price! For instance, my payment includes Private Mortgage Insurance because I have an F.H.A. Loan (we won't include house insurance in this equation). My payment is $251.40 Interest + $157.40 Principal + $89.05 Private Mortgage Insurance. Side note; you do pay more interest at the beginning of your loan then over the years it goes towards the principal.

If you calculate my total payment of $497.85 and multiply 12 months per year for 30 years, it equals $179,226.00. The purchase price of my home was $89,900.00. That is DOUBLE the actual price of the house. As bad as that sounds, owning is smarter than renting; because you build equity in your home that you can borrow or sell and get some of that money back. The only perk of renting is the landlord pays for repairs, but you don't get any return on your money. Here are a few ways to save thousands on your Mortgage.

Make Additional Principal Payments to Save Thousands

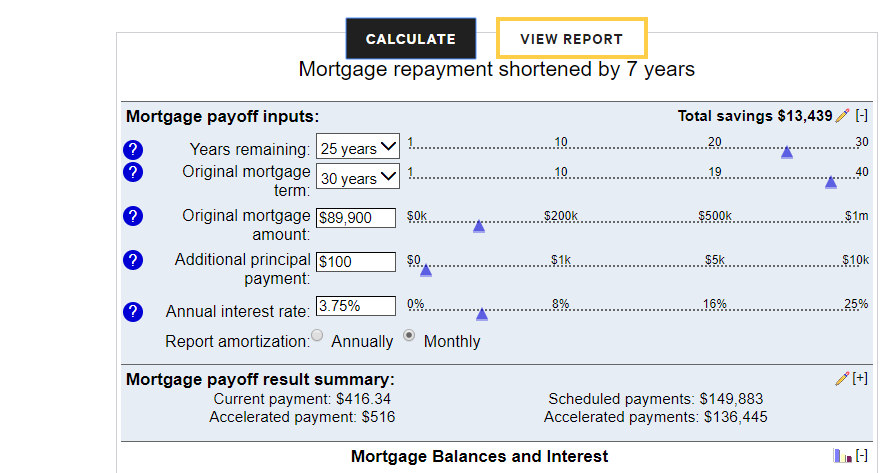

It is difficult enough to pay bills, let alone pay additional payments. Although difficult at first, you would be surprised at how much money and time you save with just a little bit extra per month. I used the Mortgage Calculator on BankRate.com (excellent site) to see exactly how much I would save on my mortgage, depending on the additional principal payments I would make. There are screenshots of the following amounts for a reference; $50, $75, and $100 of additional payments per month.

The amount of money you save along with lessening the length of the loan is shocking! Of course, you would have to go and enter your figures such as rate, balance, etc. to see what your savings would be. You can calculate yours here.

By paying only $25 extra per month, it shaves off two years and would save me $4,400! An additional $50 per month shortens the loan by four years and saves me $7,977! An additional $75 per month shortens the loan five years & 8 months, saves $10939! Are you ready for this one? By paying $100 extra per month, I would shorten my loan by seven years and save a whopping $13,439! That is a lot of money and time saved by just adding a little bit per month! I don't know about you, but I could use an extra few thousand in the bank.

Drop Private Mortgage Insurance

Private Mortgage Insurance is insurance for federally backed loans such as F.H.A. Mortgages. F.H.A. Loans are great for First-Time home buyers to get into a home for only 3.5% down payment rather than 20% for a Conventional Loan. However, you need to understand this insurance is not your Home Insurance. It is insurance for the lender just in case you foreclose on your home. They include it in your monthly payment as part of your escrow that pays taxes, insurances, and of course, their PMI.

The amount depends on your loan, of course; mine is $89 per month. Add that up over a 30-year term, and I will have paid $32,040! Just to ensure that I'm not foreclosing on my loan. The good news is once you pay your loan to 78% value of your home, you can pay for an appraisal (roughly $400 but better than thousands) and get it removed from your loan. Stay on top of this because they will not do it for you.

Refinance into a Lower Rate

The housing market fluctuates depending on factors such as interest rates, the economy, etc. If and when the time comes, and you notice a rate drop, you may consider refinancing. If you do find yourself trying to decide whether it's a money-saving move or not, there are some things to consider first.

According to an article on Investopedia.com, if you plan on selling your home in a few years, you may end up not saving anything due to closing costs that can add up to thousands plus interest if you include it into your new loan. However, maybe the rate is considerably lower at least 2%; it could save thousands if you plan on staying in your home long term.

Beware of Adjustable Rate Mortgages

Personally, this is a HUGE NO-NO! After being a victim of predatory lending, an Adjustable Rate Mortgage taught me a harsh lesson, to say the least. Back in 2006, we had refinanced our home in Florida after being convinced that an A.R.M. was a great idea. The interest rate was only 2.75%, and we could "Refinance" out of the loan at the 3-year mark when the increase would happen. Well, in 2008, the bubble burst on all the "Self-Appraised" Mortgage loans, and our home dropped 50% in value that year.

When the rate increased, our payment went from $575 to over $800 a month. Now some say it's more regulated, yet to me, it still doesn't matter. You don't know what the world will bring in 3, 5, or 10 years. You get a great low rate, then you can't refinance, or your home isn't worth what it was, and you can't even sell it. Just a nickel's worth of free advice; it's better to be safe than sorry.

I hope this information helps to inspire you to save some cash flow! (I know I will be adding some to my principle after researching this!) We all get so caught up in the paycheck to paycheck life we don't realize we have the power to keep some for a rainy day with the right information. In the end, owning your own home can be a good investment if done properly.

UPDATE: Mortgage Forbearance for COVID-19 Pandemic

Right now, you may be in a financial crisis due to the COVID-19 Pandemic. Perhaps you are a high-risk candidate for the Coronavirus and have to shelter in place due to doctors' orders, or maybe you have been laid off whether temporary or permanently from your job. Whatever the situation may be, you may want to look into the option to "pause" your mortgage payments during this crisis, depending on your lender and the type of loan you have you may qualify for a Mortgage Forbearance. For more information, check out the post "Everything you should know about mortgage forbearance" by Bankrate.

Resources:https://www.bankrate.com/calculators/home-equity/additional-mortgage-payment-calculator.aspxhttps://www.investopedia.com/mortgage/refinance/should-you-refinance-mortgage-when-interest-rates-drop-rise/https://www.bankrate.com/mortgages/everything-you-should-know-about-mortgage-forbearance/